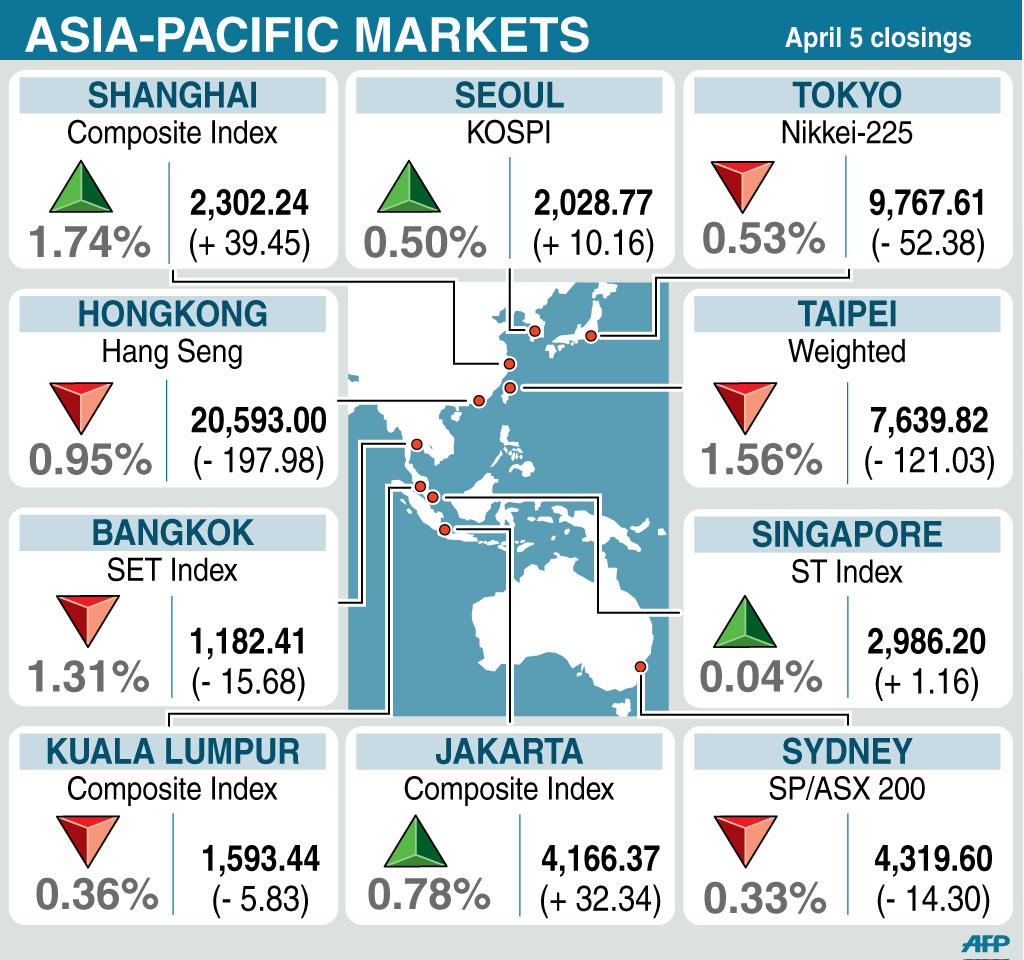

Closings for key Asia-Pacific stock markets.

HONG KONG—Asian markets were hit by renewed eurozone fears on Thursday after a weak Spanish auction raised the prospect that it could be the next country to be hammered by a debt crisis.

The news out of Madrid, as well as another batch of poor data from the eurozone, compounded downbeat sentiment after the US Federal Reserve indicated it would not provide any new stimulus to the economy in the near term.

Tokyo fell 0.53 percent, or 52.38 points, to 9,767.61 and Sydney shed 0.33 percent, or 14.3 points, to 4,319.6 while Hong Kong slipped 0.95 percent, or 197.98 points, to 20,593.00.

Taipei fell 1.56 percent, or 121.03 points, to 7,639.82.

But Seoul gained 0.50 percent, adding 10.16 points to close at 2,028.77.

Shanghai, returning after a three-day break, jumped 1.74 percent, or 39.45 points, to 2,302.24 after Beijing on Wednesday hiked the amount of cash foreigners can invest on the nation’s markets from $30 billion to $80 billion.

Chinese dealers also welcomed Sunday’s strong manufacturing data that eased fears over a slowdown in the economy.

Spain’s borrowing soared Wednesday in its first debt auction since an austerity budget last week, fuelling concern among traders of a rerun of Greece’s strife last year when it narrowly avoided a messy default.

Madrid is racing to slash its public deficit to reassure markets that it will not follow Greece – as well as Ireland and Portugal in needing a bail-out – after it missed its 6.0 percent public-deficit target last year.

Adding to the country’s problems is the fact it is heading back into recession, while the unemployment rate is tipped to hit 24.3 percent, according to government estimates.

And on Tuesday Budget Minister Cristobal Montoro warned that national debt will jump sharply to 79.8 percent of GDP this year from 68.5 percent last year.

“The rising cost of Spanish debt reignited fears in Europe as investors sold off equity investments,” Miguel Audencial, sales trader at CMC Markets, said in a note.

“Lower-than-expected European retail sales figures and German factory orders both confirmed that a full recovery is still far from reach,” Audencial said, according to Dow Jones Newswires.

The Spanish concerns come less than a week after eurozone finance chiefs agreed to boost a firewall aimed at avoiding another crisis on the scale of Greece.

Also Wednesday a study showed eurozone private sector activity retreated last month, adding to evidence that the region is in recession.

The composite Purchasing Managers Index (PMI) compiled by the Markit research firm hit a three-month low 49.1 points from 49.3 in February. A score below the neutral 50-point mark indicates contraction.

The news added to market gloom after minutes from the Fed’s most recent policy-setting meeting showed it will play a wait-and-see game before further easing monetary policy, meaning there will be less liquidity.

“Apprehensions on the future state of the US economy in a world without quantitative easing overshadowed the slightly higher-than-expected ADP employment data,” Audencial added.

Payrolls firm ADP said that while fewer jobs than expected were created in the private sector in March, figures for prior months were revised upwards.

Employment increased by a seasonally adjusted 209,000 last month, down from a revised 230,000 in February, and lower than forecasts of 217,000 net new positions. However, estimated gains for February rose 14,000, and for January by 9,000.

The figures come ahead of Friday’s key government numbers, which include the public sector jobs and the unemployment rate.

Europe’s woes overshadowed the jobs figures on Wall Street. The Dow sank 0.95 percent, the Nasdaq was down 1.46 percent and the S&P 500 shed 1.02 percent.

On currency markets the euro bought $1.3090 and 107.60 yen in early European trade, compared with $1.3141 and 108.35 yen in New York late Wednesday. The dollar was also at 82.20 yen, compared with 82.46 yen.

Oil prices bounced back from heavy losses late Wednesday in New York, where dealers staged a sell-off after the government reported a big jump in stockpiles.

New York’s main contract, West Texas Intermediate crude for delivery in May, gained 37 cents to $101.84 per barrel in the afternoon, after losing 2.5 percent on Wednesday.

Brent North Sea crude for May rose 74 cents to $123.35 08 after it shed two percent in New York.

Gold was at $1,620.90 an ounce at 0950 GMT, compared with $1,633.75 late Wednesday.

In other markets:

— Singapore closed flat, edging up 1.16 points to 2,986.20.

Real estate developer Capitaland shed 0.97 percent to Sg$3.06 while Oversea-Chinese Banking Corp. was down 0.68 percent at Sg$8.82.

— Wellington slipped 0.36 percent, or 12.44 points, to 3,467.98.

Fletcher Building ended down 0.6 percent at NZ$6.20 and Telecom shed 1.4 percent to NZ$2.435 while Chorus was 0.3 percent lower at NZ$3.46.

— Kuala Lumpur slipped 0.36 percent, or 5.83 points, to 1,593.44.

DiGi.com fell 0.5 percent to 3.91 ringgit and AirAsia fell 0.3 percent to 3.42 ringgit while Axiata Group gained 0.4 percent to 3.91 ringgit.

— Jakarta rose 0.78 percent, or 32.34 points, to 4,166.37.

Astra International rose 1.01 percent to 74,750 rupiah, Gudang Garam gained 1.40 percent to 58,050 rupiah and Sinar Mas Agro Resources added 3.97 percent to close at 6,550 rupiah.

— Bangkok fell 1.31 percent, or 15.68 points, to 1,182.41.

— Manila and Mumbai were closed for public holidays.