Our comprehensive tax reform program must really make our tax system simpler, fairer and more efficient. While we laud the government efforts in pushing for tax reform, we still need to remind our legislators to prioritize and protect our small businesses. This is due to the fact that 99.52 percent of businesses in the country are micro, small and medium enterprises (MSMEs) which employ 63.19 percent of total workforce. A number of MSMEs are registered as sole proprietors with the Department of Trade and Industry.

In an open letter to all legislators published and sent to Congress on May 2, 2020, we urged our legislators to end the injustice by legislating tax policy reforms which will help businesses adjust to the new normal and to fund the digital transformation of the Bureau of Internal Revenue (BIR).

Disparity

Last week, we published another open letter to the president to veto some provisions of the proposed Corporate Recovery and Tax Incentives for Enterprises (CREATE) bill.

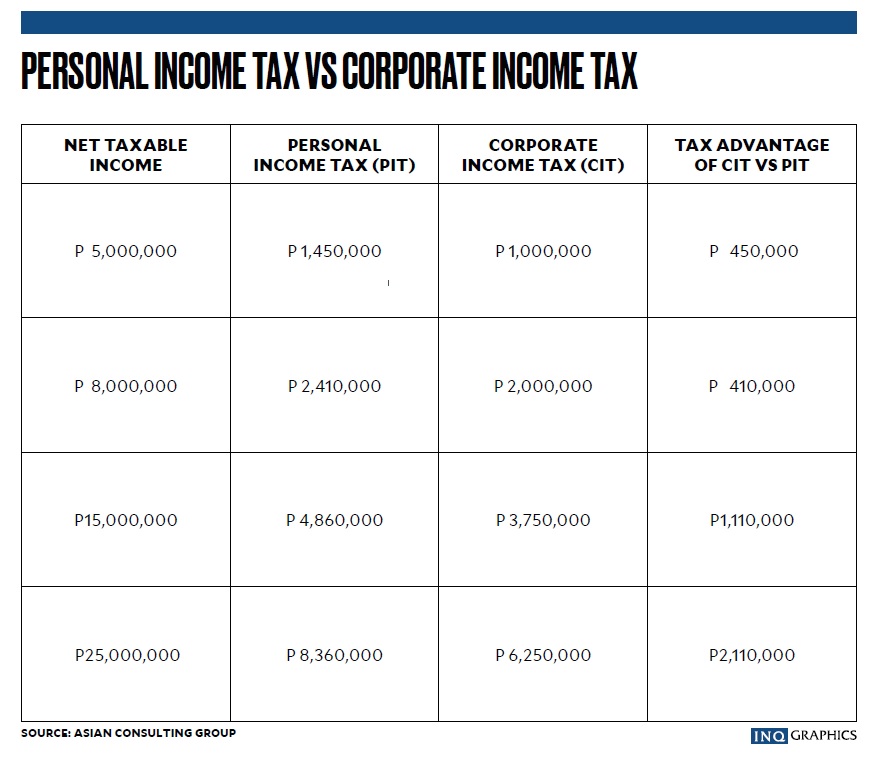

Although it will lower the corporate income tax rate from 30 percent to 20 percent, some provisions will create disparity and undue tax advantage for nonindividual (corporations) over individual taxpayers (self-employed, professionals and employees) earning P5 million and above for taxable year 2021-2022. To wit:

Under the TRAIN (Tax Reform Acceleration and Inclusion) law, individual taxpayers earning P3 million and below are considered small businesses which may avail themselves of the optional 8 percent in lieu of both income and percentage taxes. However, under the CREATE bill, small businesses are defined as corporations with net taxable income of P5 million and below and granted a lower corporate income tax of 20 percent.

Further, the TRAIN law imposes 35 percent to individual taxpayers who will earn and declare above P8 million compensation and/or net taxable income. See computation above which shows the tax advantage of nonindividual (corporations) over individual taxpayers from almost half a million to over P2 million for those with P5 million to P25 million net taxable income.

Theoretical justice

In 2027, corporations regardless of net taxable income will be paying only 20 percent corporate income tax while individual taxpayers will still pay 35 percent for earnings above P8 million as they are classified as “ultra-rich” under the TRAIN law e.g., with P30 million net taxable income an individual taxpayer will pay P9.9 million personal income tax versus P6 million corporate income tax. That’s a lot of tax advantage which defies theoretical justice of a sound tax system.

Instead of providing separate tax relief for small businesses, we should create a ax egime for small businesses which will impose a flat tax rate and simplified tax compliance for all small businesses whether registered as a sole proprietor or a corporation with threshold set not on total assets but on annual gross sales to include those in ecommerce business which may have less asset value but high gross revenues e.g., P100-million ceiling at 10-percent flat tax based on gross in lieu of income and business taxes.

Custom-fit taxation

A 10-percent flat tax will eliminate the unnecessary compliance costs and threat of BIR audit especially once the electronic invoicing has been implemented since it will be based on gross sales or revenues in lieu of income, business and other taxes.

Although our existing tax laws impose higher income and business taxes, most companies are paying barely 5 percent of their gross sales or revenues, notwithstanding the compliance costs and deficiency tax assessment during BIR audit.

Aside from the 10-percent flat tax, our legislators must also aim to broaden our taxpayer base and increase voluntary compliance from the informal sector, digital economy including startups by providing a custom-fit taxation which is simpler, fairer and more efficient for the BIR to collect taxes.

Here’s a brief discussion of the proposal:

Marginal income earners. Increase sales threshold for marginal income earners from P100,000 to P500,000, and impose fixed tax from P1,000 to P5,000 based on location, target market and years of operations to encourage all sari-sari stores, online sellers and those in the underground economy. Let them pay annually or quarterly and provide online access where they can just encode their sales and purchases for easy monitoring;

Startups. Provide a two-year tax exemption to all startups but must not be affiliated to any existing corporations or conglomerates to avoid abuse and unnecessary tax benefit to those who can afford to pay taxes already;

Small businesses. Standardize the definition of a small business whether registered as sole proprietor or corporation, use sales as threshold (not asset value) e.g., P100 million and impose a flat tax; 10-percent tax for small businesses in lieu of all other taxes i.e., income, businesses etc.;

Large taxpayers. Implement the lowering of corporate income tax from 30 percent to 25 percent, and allow them to use 20 percent but under Optional Standard Deduction;

General tax amnesty. Implement a general tax amnesty with provision on lifting of bank secrecy law for tax fraud cases so BIR can focus on high-risk, big time tax evaders.

If the goal is to make our tax system simpler, fairer and more efficient, and to provide tax relief measure especially for small businesses during this pandemic, then it’s a no-brainer to lessen the burden of taxpayers while collecting much needed revenues from those who earn more.

Creating more business opportunities is the long-term impact of a genuine tax reform. It will attract more foreign direct investments, encourage more startups and hopefully, include the informal economy to better support them without the threat of high taxes and compliance costs.

In the end, any tax policy reform must be supported by well-funded, technology-driven tax administration reform. Making it simple not just for the taxpayers, but also for the BIR to assess and collect taxes especially from the digital and new economy.

Needless to say, Congress must appropriate a significant budget to fund the digital transformation of the BIR. Given its limited budget and manpower, the BIR has exceeded its revenue collection target despite the threat of COVID-19. It has also provided several digital platforms for taxpayers to file and pay their taxes without leaving their offices or the comfort of their homes. INQ