Once again, a food price crisis has hit the country. It was so in 1995, in 2015 and this year. What seems to be wrong?

The National Food Authority, the sole rice importer/regulator, failed in its mandate of food security. But that is the short of it. The long-term challenges are more complicated that they must be understood by all stakeholders.

Food security is defined as the state in which people at all times have physical, social and economic access to sufficient and nutritious food that meets their dietary needs for a healthy and active life—Food and Agriculture Organization.

There are three main metrics: affordability, availability and food quality. The Economist Intelligence Unit developed the global food security index (GFSI), the latest was dated September 2017. The GFSI work is sponsored by DuPont.

Affordability “measures the ability of consumers to purchase food, their vulnerability to price shocks and the presence of programmes and policies to support customers when shocks occur.” It has six indicators: Food consumption as a share of household expenditure, proportion of the population under the global poverty line at purchasing power parity (PPP), gross domestic products per head at PPP exchange rates, agricultural import tariffs, presence of food safety-net programs and access to financing for farmers. This comprises 40 percent of GFSI.

Availability “measures the sufficiency of the national food supply, the risk of supply disruption, national capacity to disseminate food and research efforts to expand agricultural output.”

This examines how structural aspects determine a country’s capacity to produce and distribute food and explores elements that might create bottlenecks or risks to accessibility. The eight indicators are: sufficiency of supply, public expenditure on agricultural research and development, agricultural infrastructure, volatility of agricultural production, political stability risk, corruption, urban absorption capacity and food loss. This accounts for 44 percent of the index.

Food quality and safety measures the variety and nutritional quality of average diets, as well as the food safety. It covers the “nutritional quality of average diets and the food safety environment. Quality and safety have five indicators: diet diversification, nutritional standards, micronutrient availability, protein quality and food safety.” This composes 16 percent of the index.

Natural resources and resiliency. This category assesses a country’s exposure to the impact of a changing climate, its susceptibility to natural resource risks, and how the country is adapting to these risks.

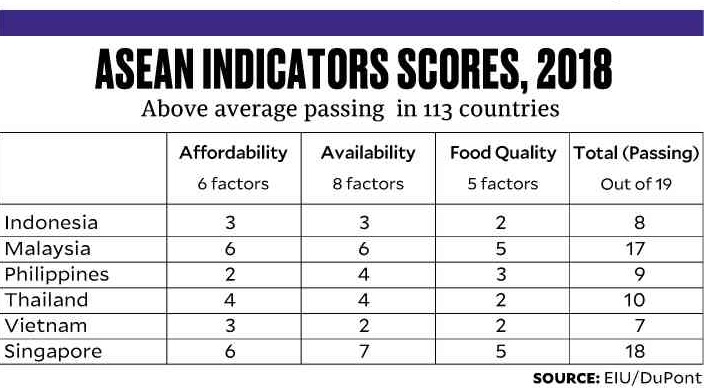

Where is the Philippines? The country belongs to the lower 65 percent of 113 countries in 2018. Among the eight Asean countries, the Philippines ranked 6th, ahead of Myanmar and Cambodia. Note that the latter are rice-exporting countries. Ranked first and second are Singapore and Malaysia, both rice-importing countries. Thailand and Vietnam, also rice exporters, followed at third and fourth. Indonesia was fifth.

Where does the Philippines falter? Among the eight Asean nations, the Philippines ranked 6th in affordability, 4th in availability and 5th in food safety.

Out of 19 indicators, the Philippines scored below average in 10: food consumption as proportion of household food spending, poverty incidence, income per capita, food safety net, farmers’ financing access, food sufficiency of supply, government expenditure on agriculture R&D, agriculture infrastructure, corruption and protein quality.

Singapore and Malaysia, both rice importers, ranked very high.

On resilience, the Philippines ranked low globally, but slightly better than Indonesia and Singapore.

Quo vadis? Relative to comparators, the Philippines failed dismally in affordability. Poverty reduction is key to food security. Of the 101 million people in 2015, some 21.6 million were poor. Nearly 17 million of these poor were rural folks with some 14 million farmers and fishers. Therefore, these groups account for two-thirds of all poor.

That means increasing incomes of farmers and fishers will solve overall poverty incidence. Since rice farmers comprise about a third, there is compelling reason to address the resource needs of the 70 percent—the nonrice farmers and fishers.

Are we food secure? From the GFSI analysis, we are not compared to our neighbors, principally from affordability (income-related) and availability (access to domestic and foreign supply). The former is due in part to high rural poverty, and the latter due in part to low productivity, limited diversification and poor agricultural infrastructure.

Given the food price crisis of 2018, the Philippines’ rank could slip in 2019.

This article reflects the personal opinion of the author and does not reflect the official stand of the Management Association of the Philippines or MAP. The author is the Chair of the MAP AgriBusiness and Countryside Development Committee, and the Executive Director of the Center for Food and AgriBusiness of the University of Asia & the Pacific. Feedback at <map@map.org.ph> and <rdyster@gmail.com>. For previous articles, please visit