Stock market savors post-election rally

WE saw them crawl back into the market three months ago, with a bit of boldness at first. Some turned jittery shortly before the May 9 presidential elections, but as they got to know the new CEO of the land better, they have since then regained control of the market.

The bulls have marched forward in a bigger way, not minding how expensive this playground has become relative to corporate earnings expectations, notwithstanding how a number of external risks loom in the horizon: Brexit (Britain’s exit from the European Union), a China slowdown, volatility in commodity prices, the US elections in November and, at some point, an increase in US Federal Reserve interest rates.

The newly invigorated bulls carried with them about P28 billion in net foreign inflows that fueled the post-election rally in the local stock market, overwhelming some P1.8 billion in net foreign buying prior to the polls.

What was previously a major overhang—-the country’s leadership turnover—turned into a positive catalyst as what historically happens during an election year. This was after Filipinos managed to pick a new President, long-time Davao City Mayor Rodrigo Duterte, in what was generally perceived as a clean, peaceful and orderly election. Mr. Duterte obtained 16 million votes, winning by a margin wide enough to dispel any doubts on the legitimacy of his mandate.

At the same time, the country posted a 6.9-percent gross domestic product (GDP) growth in the first quarter. This made it the fastest-growing economy in the region, second no more to China. And finally, Mr. Duterte pledged governance reforms, a big increase in infrastructure spending to 5 percent of GDP, ease in doing business and other measures that could bring up the country’s growth trajectory and improve the lives of the people—all of which the market liked and calmed jitters related to continuity of governance.

Upbeat view

On June 30, the day Duterte was inaugurated, the Philippine Stock Exchange index (PSEi) moved closer to the 8,000 level before succumbing to profit-taking.

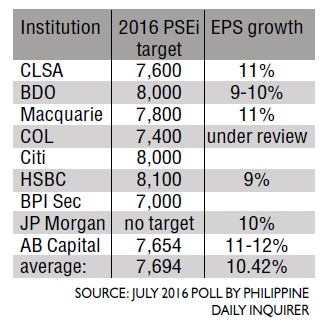

Based on official forecasts of 10 institutions culled by Inquirer, the consensus is that the PSEi will gain over last year’s finish of 6,952.08. The most upbeat view is for the PSEi to breach 8,100 while the most cautious view is for the index to pull back to 7,400.

As of the PSEi’s closing of 7,796.25 at end-June, the index has risen by 844.17 points or 12.1 percent for the year.

Consensus also points out to a growth in earnings per share (EPS) of 10.8 percent, improving from 7.4 percent EPS growth in 2015, in line with the higher growth trajectory for this election year.

In 2015, the PSEi declined by a modest 3.85 percent.

In terms of valuation, the PSEi ended June at more than 20 times EPS this year, which means investors are paying 20 times the amount of money they expect to make. This is seen as a high valuation relative to a historical price-to-earnings (P/E) ratio only 14x to 15x and the five-year average of 17.5x.

AB Capital Securities analyst Victor Felix said the post-election bull run was ignited not because of Duterte per se but because the new President had received a clear margin of victory alongside perceptions of clean and honest elections and the strong first-quarter GDP growth.

“Net foreign transactions have diverged in May when the index surged post-elections to retest the 7,500 level. We view the divergence as a bullish indicator as local investors have a more steady hand compared to foreign investors,” Felix said.

10-point agenda

The first 100 days of Mr. Duterte’s administration is seen very crucial in terms of assessing whether he could deliver on the 10-point socioeconomic agenda which the market has generally welcomed.

Continuing and maintaining the current macroeconomic policies, including fiscal, monetary and trade policies;

Instituting progressive tax reform and more effective tax collection while indexing taxes to inflation, in line with the plan to submit to Congress a tax reform package by September;

Increasing competitiveness and the ease of doing business, drawing upon successful models used to attract business to local cities such as Davao, as well as pursuing the relaxation of the Constitutional restrictions on foreign ownership, except with regards land ownership, in order to attract foreign direct investments;

Accelerating annual infrastructure spending to account for 5 percent of the gross domestic product, with public-private partnerships playing a key role;

Promoting rural and value chain development toward increasing agricultural and rural enterprise productivity and rural tourism;

Ensuring security of land tenure to encourage investments and address bottlenecks in land management and titling agencies;

Investing in human capital development, including health and education systems, as well as matching skills and training to meet the demands of businesses and the private sector;

Promoting science, technology and the creative arts to enhance innovation and creative capacity toward self-sustaining and inclusive development;

Improving social protection programs, including the government’s conditional cash transfer program, in order to protect the poor against instability and economic shocks, and Strengthening the implementation of the Responsible Parenthood and Reproductive Health Law to enable, especially, poor couples to make informed choices on financial and family planning.

“Under Duterte’s leadership, we believe the ’change coming’ would mean more innovative ways in doing things as government faces up to the usual challenges of reducing poverty, plugging infrastructure gaps, fighting criminality and winning the war on drugs that, hopefully, would yield a fairer distribution of income benefits over time,” said Jun Trinidad, economist at Citi Philippines, in a July 7 research note titled “Seeking New Ways to Fixing Old but Recurring Problems.”

“Desired results may only be known several months from now but the mix of process change and bold ideas coming from Duterte’s team to address recurring problems and issues, instead of the usual slate of customary fixes and remedies, appear to embolden the outlook,” he pointed out.

Local investment house First Metro Investment Corp. sees the PSEi challenging this year the record high level of 8,127 seen in April last year. This is on the back of “rock-solid” underlying macroeconomic backdrop and higher infrastructure spending that bode well for corporate earnings, FMIC assistant vice president Cristina Ulang said.

Infrastructure spending

Ulang said President Duterte’s “quite aggressive” plan to boost infrastructure spending to 5 percent of GDP would be a strong catalyst for the market. The government has not seen such kind of infrastructure spending since the Macapagal-Arroyo administration, she said. During the Aquino administration, infrastructure spending fell to as low as 1-2 percent of GDP (as the administration prioritized governance reforms) before rising to 3.5 percent last year.

“Our earnings growth is not as impressive but we continue to have good fundamentals on account of low inflation, good liquidity in the system and strong banking system with sufficient capitalization which are supporting earnings growth moving forward,” Ulang said.

‘Special’ year

But this year is particularly a “special” year given that elections—based on history—always boosted the economy. Every first quarter of all four past election years had seen a 7.3 percent quarterly growth in expenditure compared to an average of only 4.5 percent during non-election years. The quarterly GDP upside for the second quarter typically averaged at 8 percent compared to only 4.8 percent during the non-election years, Ulang noted.

At the same time, the increase in the Philippines’ weight in the closely tracked MSCI index and the inclusion of Security Bank in the main index had likewise boosted investors’ confidence alongside rising bets that the US Federal Reserve may not longer hike interest rates too soon.

“This is one basis why the stock market has flown to where it is now,” she said.

Summing up what the market would like to see in the next six years (See related story on page B3-4), it would be to sustain a higher economic growth trajectory, keep or even improve the government’s investment-grade rating, deepen drive against corruption, ease doing business, honor the sanctity of government contracts, invest more in infrastructure and continue the PPP program, develop new sources of growth and liberalize the economy through constitutional amendments.

Overweight

British banking giant HSBC is among those institutions with an “overweight” recommendation on Philippine equities. “Overweight” is a recommendation to increase allocation relative to the benchmark, usually the MSCI Asia ex-Japan index.

“We remain overweight on the Philippines on a regional basis. The country’s macro health is impressive, driven by strong, domestic consumption-led growth. The recent presidential election that saw Rodrigo Duterte emerge victorious has reduced uncertainty and improved sentiment. Meanwhile, we believe there is ample room for growth in the equity market, with mutual funds positioning near neutral levels,” Herald Van Linde, HSBC head of equity strategy for Asia Pacific, said in a June 30 research note.

Growth expectation

The Philippines, which shed its “sick man of Asia” stigma only in the last six years, still has a meager weight of only 1.9 percent in MSCI Asia ex-Japan compared to the 4.9 percent weight for Singapore, 3.5 percent for Malaysia, 3.1 percent for Indonesia and 2.7 percent for Thailand. China has a weight of 30.5 percent while the respective weights for Korea, Taiwan and Hong Kong are 17 percent, 14.2 percent and 12.3 percent. India has a weight of 9.9 percent.

Van der Linde said the new administration’s economic and business agenda could lead to more comprehensive development and further support the country’s growth outlook.

While the consensus forecast for the earnings has come down since the start of the year, the HSBC analyst said EPS growth expectation for 2016 was still one of the highest in the region, he said. “Also, earnings momentum has turned positive in June, following three months of negative readings. As such, we believe risk of any more consensus forecast declines looks unlikely in the near term.”

Major concern

HSBC’s only major concern on the local market is its steep valuation. At a P/E ratio of about 19x, the equity market trades at an 8-percent premium to history and at a 55-percent premium to the regional average, which Van der Linde said could put a cap on the rally.

Among sectors, HSBC prefers consumer companies with impressive balance sheets. It also likes the infrastructure sector, expecting the PPP program to gather pace under the new government, which is seen to benefit related companies. However, HSBC said it believed that issues such as restriction on foreign ownership and disputes on water and toll-road tariffs need to be resolved soon. HSBC also expects electric utilities to benefit from the growing opportunities in the retail market. “As many as 17 companies are in this market as it offers access to large, credit-worthy customers and a less regulated tariff regime. In addition, generation utilities also see an opportunity to grow their market shares as older capacities are retired,” the research note said.

Underweight

Citi equity analyst Joahnna See, in a research note dated July 1, said the country’s macroeconomic fundamentals remained favorable, with GDP growth likely to accelerate to 6.3 percent this year and further to 6.5 percent in 2017 from 5.8 percent last year. “Positive legacy issues from the outgoing Aquino government and favorable policy signals from the incoming Duterte government bode well for annual growth of over 6 percent,” See said.

“Duterte’s Cabinet appointees largely comprise ex-officials of the Arroyo, Ramos and Aquino governments, including his Davao-based supporters. Most of the appointees are seen as stronger managers than big-picture thinkers,” See said.

The Citi analyst said the impact of Brexit would largely be limited to “portfolio effect” as risk-off sentiment in global markets would not spare the Philippines, adding that exposure to bilateral trade with and investments from the UK were minimal. Downside risk to Brexit’s impact on GDP could be channeled through lackluster remittances from the UK (See related story on page B6-1).

Citi, however, has an “underweight” rating on Philippine equities, noting that market valuations were “not yet compelling.”

Nonetheless, Citi said the risk of sharp foreign outflow had been reduced as net selling as a percentage of turnover was near historical lows in 2015.

See also noted that earnings recovery was underway for Philippine equities, led by banks, property, consumer and conglomerates.

“Key earnings risks include competitive pressures eroding top-lines and margins, weaker credit growth and volatile bond markets in the banking sector, and lower property leasing take-up,” See said.

Risk factors

But even as blue skies are there for now, there are risks over the horizon. The aging bull has been reinvigorated but Brexit, a China slowdown, the US elections and volatile commodity prices remain key triggers for increased investor risk. For now, prospects of the US raising interest rates have diminished especially as Brexit is seen to remain a source of uncertainty in the next two years.

“Brexit is bad for all asset classes except gold, which is a safe haven, and also the yen,” said AB Capital Securities’ Felix, who expects regional equities to decline by 4-10 percent.

The good news was that most Philippine companies have limited exposure to EU and any dip would be an opportunity to accumulate, Felix said.

Meanwhile, the US elections this November could be another source of fresh uncertainty given the big impact of US leadership on global economic and political affairs. Republican candidate Donald Trump and the Democrats’ Hillary Clinton are vying to be the next president of the world’s biggest economy.

Political risks

Domestically, political risks have diminished but not fizzled out. Can Mr. Duterte deliver on his promises and bring the country to a higher growth trajectory? Can the new President build much-needed infrastructure and strengthen institutions while keeping the investment-grade rating intact? Can the domestic economy grow fast enough to allow corporate earnings to catch up with lofty valuations?

COL Financial, which is expecting a yearend PSEi level of only 7,400, sees local stocks giving up recent gains for the rest of the year.

“We are hopeful that there will be pullbacks,” said COL head of research April Lee-Tan. “August is historically a weak month, plus there’s Brexit and expensive valuation at 20x P/E.”

Strong growth momentum

Felix said what was important would be if the country could sustain a strong growth momentum, say 6.9-7 percent GDP growth rate for the second quarter, which would be key to sustain the market’s rise.

”Our index is comparatively more expensive than other indices, though this is justified considering our GDP growth rate and other positive domestic factors,” Felix said.

Carlos Ma. Mendoza, executive director and head of banking for JP Morgan Philippines, said even if the US Federal Reserve were to keep interest rates low for longer, this second half would be quite volatile because of the uncertainties over “Brexit.”

“There’s a flight to quality. Everyone has his or her own definition of quality but people are looking for strong stories and I would argue that we have a strong story to convey,” Mendoza said. TVJ